{kind=link}

2023 has been a yr filled with ups and downs. If somebody had informed me at first of the yr that we’d see the Russia-Ukraine struggle proceed into its second yr, and that October would see Israel launch a full-blown assault on Gaza main to fifteen,000 lives misplaced in below 2 months…I’d have discovered it onerous to imagine.

However that’s precisely what occurs – Life usually has its means of peculiar us.

As 2023 involves an finish, that is my annual evaluate of my funds to test the place we are actually and be certain that we’re not falling too far off from our targets. Throughout this yearly evaluate, I usually study my earnings development, bills, financial savings, insurance coverage protection, and funding efficiency – which helps me to raised strategize for the brand new yr.

Time flies, this marks the tenth yr that I’m doing this on the weblog! Earlier than I am going into this yr’s evaluate, right here’s a fast recap of earlier years:

- 2014: Saved $20,000

- 2015: Saved $30,000 and grew earnings

- 2016: Saved $40,000 and grew earnings, hit $100k in web price at age 26 together with CPF

- 2017: Saved $45,000 and doubled my web price in a yr

- 2018: Saved $50,000

- 2019: Saved $35,000 (didn’t realise I fully missed out on a round-up submit, however right here’s our child-related bills as a substitute)

- 2020: Saved $30,000 and achieved loopy (irregular) funding returns

- 2021: Saved $40,000, grew earnings however noticed decreased funding returns

- 2022: Saved $45,000 and battled a bearish funding local weather

Financial savings & Earnings

This yr’s financial savings hit an all-time excessive, largely fuelled by the expansion in my earnings – which greater than made up for increased family bills as a result of inflation.

| 2014 | $20,000 |

| 2015 | $30,000 |

| 2016 | $40,000 |

| 2017 | $45,000 |

| 2018 | $50,000 |

| 2019 | $35,000 |

| 2020 | $30,000 |

| 2021 | $40,000 |

| 2022 | $45,000 |

| 2023 | $60,000 |

Loyal readers may recall how I selected to take a step again in my profession after welcoming my second child. In 2021, I gave up my Director position and was headhunted to affix a competitor, the place I requested for a less-demanding Senior Supervisor position as a substitute, clocking in simply 3 days every week (and extra throughout crunchtime). However in 2023, I bought promoted to a brand new portfolio as Director, working intently with the federal government on new insurance policies and I now handle a crew chargeable for bringing in and sustaining an enormous bulk of our firm’s Singapore income base.

Consequently, my salaried earnings doubled.

My facet hustles have additionally continued as BAU (enterprise as common), however I seen one thing highly effective kick on this yr: the ability of referrals. Phrase in regards to the work that I do (for weight reduction) actually began spreading as my preliminary base of consumers (who efficiently misplaced weight) shared their “secret” with their family and friends members, which resulted in referrals and loads of new enterprise from of us who by no means in any other case heard of me (or Price range Babe).

Subsequent yr, I’m trying to construct one other new supply of earnings, so we’ll see if that kicks off!

Bills

Because of inflation and rising costs, our household bills have risen considerably. We bought hit by a better mortgage price (since we opted for a financial institution mortgage once we signed our mortgage pre-COVID at 1+%) and increased family payments on the identical time, identical to everybody else who’s a home-owner and pays for his or her household in Singapore.

Our present month-to-month family earnings has risen to:

| Nate: childcare & enrichment | $1,200 |

| Finn: childcare & enrichment | $1,000 |

| Helper wage and levy | $1,000 |

| Mortgage & dwelling insurance coverage | $1,300 |

| City council, carpark and utilities | $650 |

| Eating & groceries | $1,400 |

| Household insurance coverage insurance policies | $1,200 |

This excludes our particular person eating bills, the allowances that we give to our dad and mom (a 5-figure sum annually) and different miscellaneous bills that aren’t recurring in nature, so you may think about how the precise sum is rather a lot increased.

Our payments (mounted bills) have gone up, however the greatest ache has positively bought to be from the price of consuming out, which has elevated considerably as F&B retailers hiked their costs this yr. To adapt, we’ve been making an attempt to chop down on this so as to not bust our funds (though it’s onerous to run away from it completely, particularly when you might have youngsters who request to eat at sure locations on weekends).

For abroad travels, we introduced our household (and fogeys) to Taiwan for a 2-week journey and spent 4D3N in Cameron Highlands, so our complete vacation funds rose from $5k final yr to $13k this yr.

Insurance coverage

My husband and I added 2 new insurance coverage insurance policies this yr to our portfolio to extend our protection for important sickness, particularly after MOH dominated that most cancers will now not be lined 100% below typical insurance policy.

We misplaced a number of mates to demise this yr and noticed a number of others bought identified with most cancers, so we determined to behave whereas we’re nonetheless in good well being.

Investments

However you understand what was much more sudden?

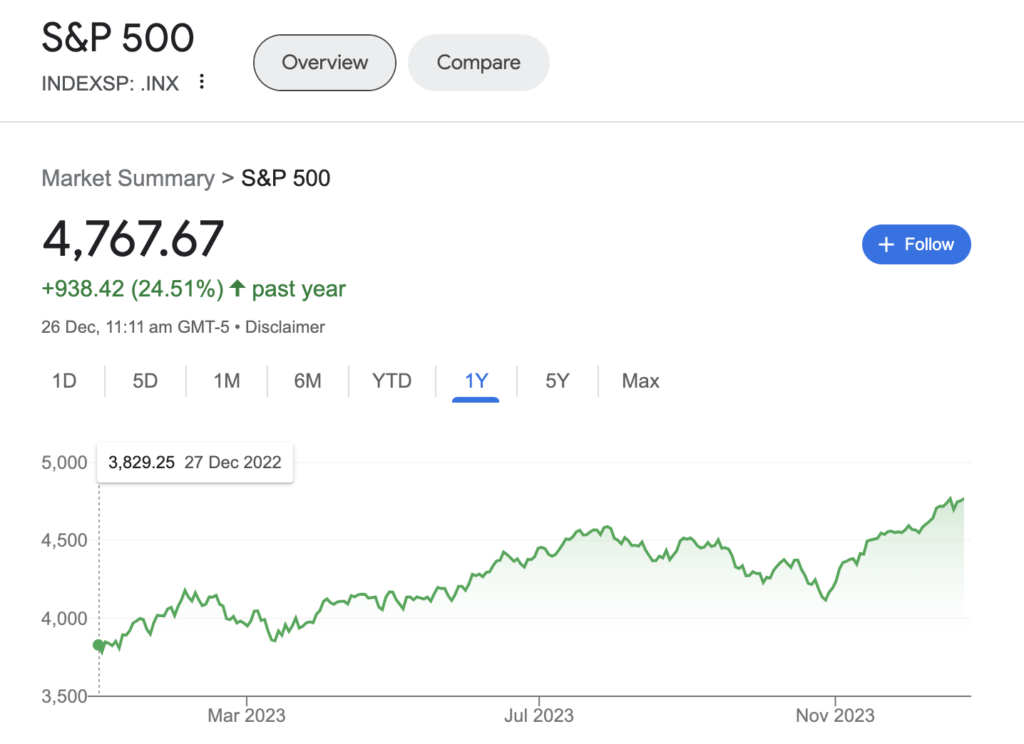

That the inventory market would formally backside out in December 2022 and see the beginning of a brand new bull ushered in by ChatGPT’s launch (on 30 Nov 2022, marking the stellar rise of Synthetic Intelligence shares (and hype?).

And that the S&P 500 would go on to achieve 25% in 2023 alone, principally pushed by mega-cap shares together with Microsoft, Apple, Alphabet, (new-darling) Nvidia and Meta, and many others.

When you had diligently caught to your investing all through (as a substitute of giving up like what most retail buyers did, when the bear market triggered by the tech shares crash in 2022 continued for for much longer than most individuals anticipated)…congratulations, you’d have seen your portfolio transfer from being within the purple to into the inexperienced.

After I wrote this final yr,

“In complete, my funding portfolio is at the moment down by about ~35%”.

SG Price range Babe, 30 December 2022

I actually wasn’t anticipating the market to reverse so quickly and for my portfolio to return into the inexperienced so rapidly, however that’s precisely what occurred.

On one other good observe, my dividends payout have additionally hit an all-time excessive this yr, with a major enhance coming from DBS’ hike earlier.

All in all, my investments are again on monitor.

Conclusion

I’m shocked that my financial savings hit a brand new milestone this yr – contemplating how the final time I hit $50k was earlier than I had youngsters, I actually wasn’t anticipating to surpass the quantity this yr as a result of inflation.

However that’s the ability of elevated incomes capacity. If something, this yr has really been reminder that we must always proceed to work onerous and construct by means of our 20s and 30s, in order that we are able to have a better time in our later years.

After I began this weblog in 2014, I wrote that my purpose was to retire by age 45. Taking a look at my very own monetary report card and progress since then, it’s protected to say that barring any sudden occasions, I’m nicely on monitor to attaining it.

My 2023 monetary abstract would thus be:

- increased earnings (as a result of a promotion at work, and extra referrals),

- increased bills (as a result of inflation),

- a extra resilient insurance coverage portfolio, and

- improved funding efficiency (because the inventory market turned bullish).

The subsequent huge merchandise on my monetary agenda will likely be to construct my dividends portfolio to the purpose the place my dividends will likely be sufficient to pay for my residing bills. I estimate that this may take me 2 – 4 years to execute, so I’ll replace as soon as I clear that milestone.

See you guys over within the new yr!

With love,

Price range Babe