{kind=link}

1. Mortgage charges will transfer decrease and hit the 5s sooner or later

I all the time begin my New Yr predictions submit with a guess about which means mortgage charges will go.

It’s very troublesome to foretell mortgage charges and nearly no person will get it proper. However we will make some educated guesses based mostly on what we all know.

Complicating 2025 is a brand new incoming presidential administration. And never simply any, however a second time period for Donald Trump.

This time round, he has promised some sweeping adjustments, together with widespread tariffs, mass deportations, and large tax cuts.

All three spell increased inflation, which is what the Federal Reserve has been battling since at the very least early 2022.

They’ve made a variety of progress, however there are fears Trump’s insurance policies might unwind that in a rush.

That is partially why 10-year bond yields, that are used to find out mortgage charges, have risen a lot lately despite three separate Fed price cuts.

Nonetheless, there’s additionally rising unemployment and fears of a recession, which might counteract a few of Trump’s inflationary insurance policies.

There’s additionally the concept he could not really do what he stated he would do. For me, the financial knowledge will matter extra and I see the economic system slowing and starting to battle.

That’s not excellent news for the economic system, clearly, but it surely could possibly be excellent news for mortgage charges.

Like previous years, they gained’t transfer in a straight line down, however I do consider they’ll be decrease in 2025 than in 2024, with a 5-handle an actual chance.

Simply anticipate a variety of volatility alongside the best way and act quick if you want to lock your price!

Learn extra: 2025 mortgage price predictions

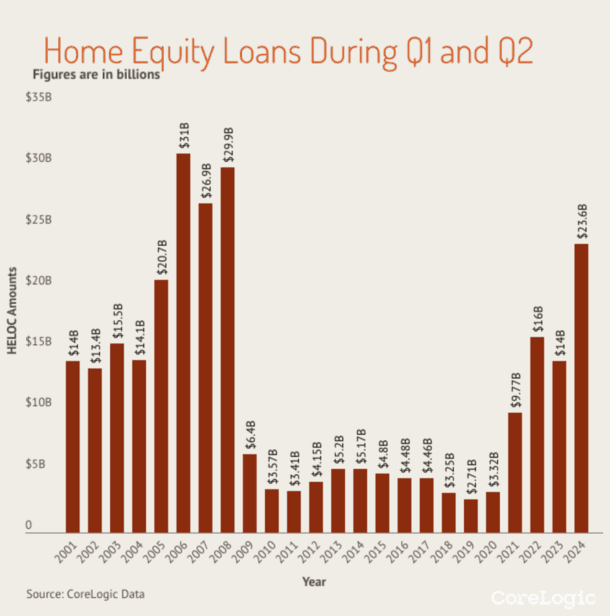

2. Second mortgages will get much more in style as customers want money

Whereas second mortgages have gained in recognition in recent times, largely as a consequence of first mortgages being rate-locked at very low ranges, they nonetheless haven’t had their second.

And by second, I imply when everybody and their mom takes out a dwelling fairness mortgage or dwelling fairness line of credit score (HELOC).

That second might are available in 2025 for just a few completely different causes. For one, current householders are sitting on document dwelling fairness with very low loan-to-value ratios (LTVs.)

Secondly, they’ve burned by way of their extra financial savings and can need (or must) preserve spending. These mortgages will enable them to just do that.

Lastly, mortgage servicers are targeted on current householders of their portfolios and will probably be pitching them stated merchandise, figuring out a primary mortgage isn’t an possibility for many.

Mortgage lenders may even want to do that to remain afloat if mortgage charges stay stubbornly excessive and forestall them from originating enough buy and refinance quantity to maintain the doorways open.

So in the event you’re a house owner, anticipate to be pitched one in every of these loans.

Should you’re an economist, control this sort of lending. If it turns into rampant, we’ll have a riskier housing market with extra leverage and debt, amid doubtlessly plateauing dwelling costs.

Tip: Three Key Variations Between HELOCs and House Fairness Loans

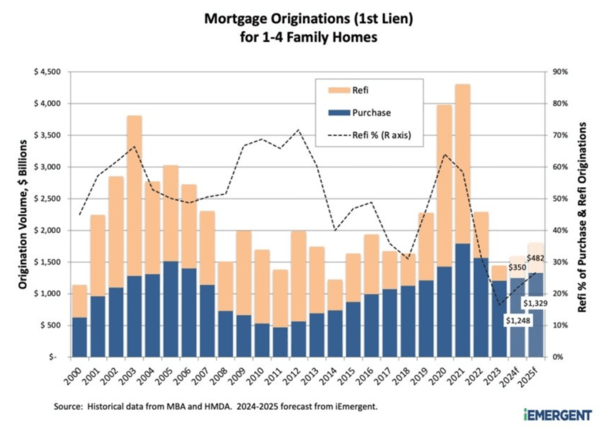

3. Refinancing will decide up steam as charges fall and lenders pounce

Mortgage lenders have been ready with bated breath for mortgage charges to fall. They usually may wish to take a breath as a result of it appears to be taking without end.

Whereas we did get a pleasant price reprieve again in August and September, charges shot increased once more and at the moment are nearer to 7% once more.

But when/once they fall again towards 6% in 2025, and even into the 5s, there will probably be a fairly sizable refinance increase.

Individuals preserve throwing out the phrase “mini refi increase” since it will pale compared to the price and time period refinance increase seen from 2020 to 2021.

Nonetheless, it’d nonetheless be a fairly impactful occasion for the mortgage officers, mortgage brokers, and lenders on the market making an attempt to drum up enterprise.

A latest report from iEmergent stated refinance quantity is anticipated to rise one other ~40% in 2025 after climbing about 50% from 2023.

And a few 5 million refinance purposes hinge on mortgage charges falling again to round 5.5%.

So charges can actually make or break the mortgage market subsequent 12 months and will probably be essential to control.

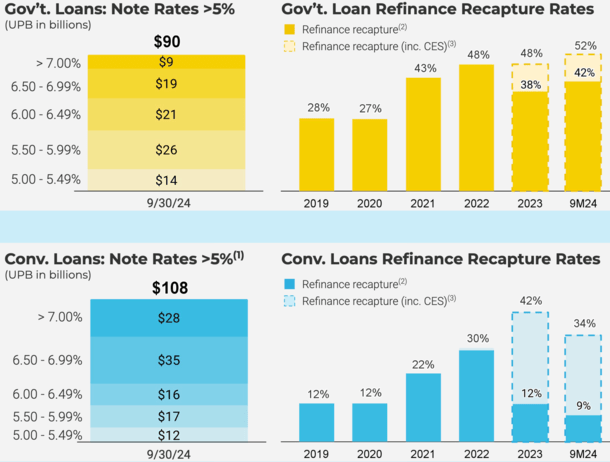

4. Recapture will probably be the secret for brand new mortgage originations

Should you haven’t heard of recapture, you’ll. It has develop into all the trend within the mortgage world.

As an alternative of on the lookout for new prospects, lenders and mortgage servicers are merely scanning their current consumer database to search out new enterprise prospects.

Due to improved expertise, this course of may be automated so anybody of their rolodex will probably be alerted if they will profit from a refinance or the addition of a second mortgage.

In September, the nation’s largest lender UWM launched KEEP to assist its brokers retain their shoppers, even when the servicing rights to these loans lie with one other firm.

This development has partially been pushed by the shortage of latest enterprise on the market, forcing mortgage originators to return and work with what they’ve obtained.

Should you’re a house owner, don’t be shocked in case your lender reaches out to you earlier than you attain out to them.

And even when their provide sounds nice, all the time take the time to comparability store it with competing brokers and lenders.

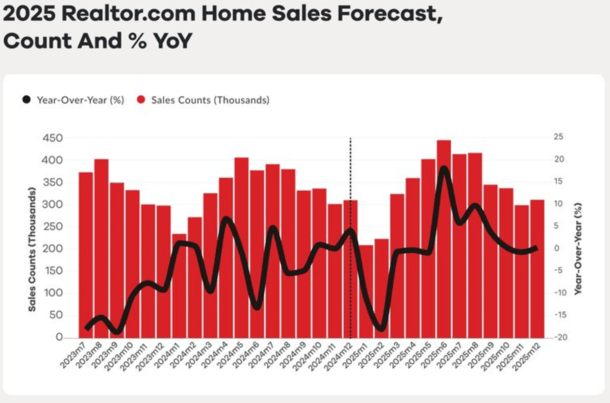

5. House gross sales will bounce off the underside however not enhance as a lot as folks assume

There’s been a variety of optimism that 2025 might usher in a 12 months of a lot increased dwelling gross sales as these on the fence lastly soar in.

The thought is that customers are accustomed to excessive mortgage charges now and are sick of ready.

It’s an excellent thought, however as soon as many of those of us runs the numbers, they could balk, even when they wish to purchase a house.

The value of property taxes and householders insurance coverage, coupled with a better mortgage price and a still-high asking worth simply may not pencil.

It’s nonetheless not even clear if we’ll surpass 4 million current dwelling gross sales for 2024, which might develop into the underside for gross sales this cycle.

However chances are high 2025 will see gross sales above the 4 million threshold, although maybe not by a large margin.

In different phrases, 2024 will possible show to be all-time low for gross sales, and 2025 will probably be a bit higher, however not significantly better. As seen within the chart above from Realtor.

In fact, surprises are all the time doable and if there actually is pent-up demand from impatient consumers, it might end up higher than anticipated.

6. House worth positive factors will probably be muted regardless of higher charges

Whereas I do anticipate mortgage charges to proceed their downward trajectory into the brand new 12 months, I don’t anticipate it to correlate to even larger dwelling worth positive factors.

Whereas 2024 will possible see dwelling costs up over 5% once more, 2025 will in all probability see a continued deterioration within the price of appreciation.

In different phrases, anticipate dwelling costs to go up once more in 2025, however solely by 2-3% as an alternative of 5%.

Lengthy story brief, actual property is dear! There’s no option to sugarcoat it anymore, and with rising provide and never a ton of consumers, effectively, anticipate costs to ease.

This can fluctuate by area, with states like Florida and Texas anticipated to be cool once more because the Northeast and Midwest possibly outperforms.

Both means, I wouldn’t financial institution on a giant worth hike with values trying fairly topped out nowadays in most locales.

For dwelling consumers, this may be a plus if the vendor is extra keen to barter or throw in vendor concessions.

They might even be extra keen to pay your agent’s fee too!

7. Actual property agent commissions will come down as extra negotiate

I’m hoping we get extra readability on the continuing actual property agent fee drama that unfolded in late 2024.

New guidelines don’t enable presents of compensation on the MLS and it’s now not a assure that the vendor or itemizing agent will cowl the customer’s agent compensation.

As such, both the customer has to foot the invoice or they should negotiate with the vendor to pay it. Word that actual property commissions can’t be financed instantly.

Given it’s now not a certainty, I anticipate commissions to fall additional in 2025, although it should depend upon the transaction in query.

Merely put, if the house is much less in demand, the vendor may be keen to supply the complete 2.5% or 3% to the customer’s agent to maneuver it shortly.

Conversely, if it’s a scorching property with a number of bidders, a purchaser may must foot the invoice and negotiate a decrease fee to their agent.

This may entail telling their agent they will solely pay 2% or 1.5%. The secret is that must be negotiated upfront.

A technique as a house purchaser may be to supply your agent their full 2.5%, however inform them if the vendor solely presents X, that’s all they get. You gained’t make up the distinction!

Learn extra: It’s okay to barter together with your actual property agent!

8. Extra actual property/mortgage corporations will embrace the vertical mannequin

We’ve seen extra corporations attempt to do all of it in the true property/mortgage area, and we’re possible going to see extra of it in 2025, particularly if there’s a friendlier regulatory local weather.

For instance, Zillow isn’t happy with simply being a portal the place you may search for your Zestimate.

Additionally they need your own home mortgage, as evidenced by their large hiring spree at their affiliated Zillow House Loans unit.

Different lenders proceed to include their very own settlement companies in-house, or launch actual property agent referral techniques.

Merely put, corporations wish to seize an even bigger piece of the general transaction, as an alternative of simply the mortgage, or the agent piece, or the title and escrow.

The identical has been taking place with dwelling builders, with the builder’s lender usually beating out the competitors for the mortgage too.

Builders wish to management extra of the method to make sure the mortgage will get to the end line. They’ll additionally make more cash that means too. Win-win.

However once more, be sure as a client you’re successful too and never simply paying extra for the comfort of one-stop procuring.

9. FHA premiums will probably be lower (and possibly life-of-loan insurance policies too!)

Right here’s one prediction that would make homeownership a tad bit simpler. I anticipate the FHA to chop premiums in 2025.

And presumably do one thing about that pesky life-of-the-loan insurance coverage coverage the place mortgage insurance coverage can by no means be canceled, even with a really low LTV.

The FHA’s Mutual Mortgage Insurance coverage Fund (MMI Fund) could be very effectively capitalized and premium cuts at the moment are warranted given the buffer over the minimal reserves required.

And whereas Trump obtained in the best way of a FHA lower throughout his first presidential time period as a result of wished much less of a authorities footprint in mortgage, I don’t assume he’d be opposed this time round.

He is aware of housing is high of thoughts for People and can wish to make it cheaper for them. This could possibly be a straightforward option to obtain that and take a fast win himself.

Chances are high a 25-basis level lower to premiums on FHA loans wouldn’t make or break many offers, however each little bit helps. Maybe the upfront premium is also lowered.

If the life-of-the-loan coverage was eliminated, it’d be an enormous blessing to current FHA holders, assuming they might cease paying the pricey premiums.

Keep tuned on this one!

10. Fannie and Freddie will stay in conservatorship

Lastly, whereas there have been a variety of rumblings recently, as there have been eight years in the past when Trump was first elected, I don’t anticipate Fannie Mae and Freddie Mac to be launched.

Whereas it’s maybe an excellent thought and one thing that ought to be carried out, given they’ve been in authorities conservatorship since 2008, I don’t see it taking place.

There has already been a variety of blowback, with of us arguing that mortgage charges could be even increased with out a authorities assure from Fannie and Freddie.

We’re additionally in a tenuous a part of the cycle with dwelling costs capping out and affordability traditionally fairly poor.

Twiddling with the mortgage finance spine may be ill-advised timing-wise. And once more, Trump will need the bottom mortgage charges doable for America.

So jeopardizing that with the discharge of Fannie and Freddie again into the wild looks as if a dangerous endeavor.

However once more, something is feasible and I don’t anticipate 2025 to be a quiet, surprise-free 12 months by any stretch of the creativeness.

So that you may wish to buckle up and put together for the worst, however hope for one of the best. And keep vigilant if shopping for a house, promoting a house, or a taking out a mortgage!

Earlier than creating this website, I labored as an account government for a wholesale mortgage lender in Los Angeles. My hands-on expertise within the early 2000s impressed me to start writing about mortgages 18 years in the past to assist potential (and current) dwelling consumers higher navigate the house mortgage course of. Comply with me on Twitter for warm takes.