{kind=link}

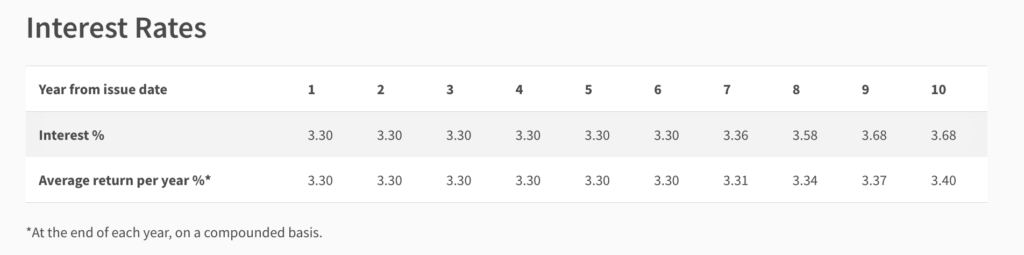

Announcement: If you happen to haven’t seen it but, the most recent Singapore Financial savings Bonds yield 3.4% over 10 years, which is the best yielding SSBs for all of 2023 until date!

That is additionally one of many highest since SSBs had been launched, with a couple of exceptions equivalent to final 12 months’s December 2022 tranche, which yielded a barely larger return of three.47% within the unsure rate of interest local weather again then.

At this fee, SSBs at the moment are extra enticing than different short-term risk-free choices equivalent to banks’ mounted deposits or MAS Treasury Payments. The issue with these 2 different devices is that they’ve a shorter time period period, which implies it’s important to hold discovering new locations to place your funds in after 6 months / 1 12 months / 2 years. For these of you who haven’t any time to maintain buying round for various choices, then this month’s SSB would possibly simply be your reply.

Right here’s the rates of interest for this month’s SSB over the subsequent 10 years:

What I like in regards to the Singapore Financial savings Bonds

The large profit with SSBs is that you lock in rates of interest for 10 years. If rates of interest are going to get slashed in 2024, this provides you the choice of holding onto a better yield by way of this month’s SSB.

Yields apart, the subsequent smartest thing about SSBs are in its liquidity since you solely want to attend for 1 month to liquidate your funds. At any time once you want the money again, you may get it inside the begin of the next month.

The minimal sum can be pretty low, beginning at simply $500 and in multiples of $500. The utmost quantity of SSBs you possibly can maintain at anyone time (together with from earlier months’ tranches) are capped at $200,000.

SSBs are additionally backed by the Singapore authorities, making it a fairly risk-free selection for these of you who’re tremendous risk-adverse. There could also be different larger yield choices in at this time’s market, however do observe that these aren’t risk-free:

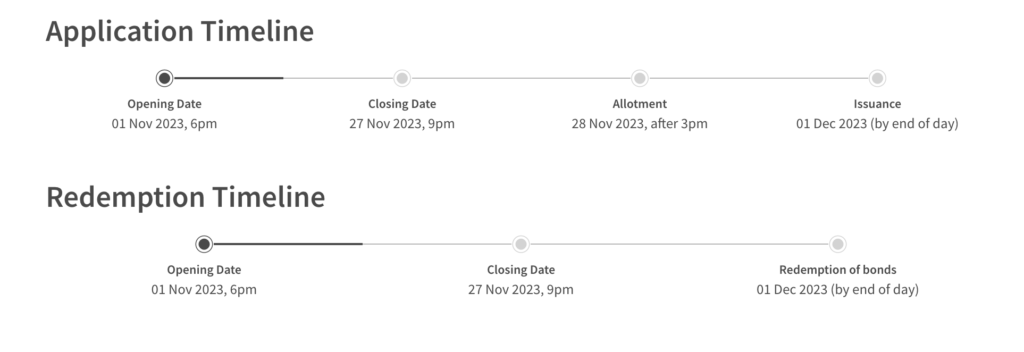

The applying timeline may be discovered beneath, or right here at the official SSB hyperlink:

If you happen to’re intending to use, you are able to do so by your DBS/POSB, OCBC or UOB web banking portals or ATMs. And in case you intend to make use of your Supplementary Retirement Scheme (SRS) funds as a substitute, then you definately’ll have to make use of the web banking portal of the financial institution the place you could have your SRS funds deposited in.

The one value is the $2 utility payment and some minutes to get it arrange by way of web banking.

Word: You can't use your CPF funds to purchase SSBs.

Share this with anybody you recognize who would possibly need to take a look at this month’s bond.

For extra particulars, chances are you’ll cross-verify on the official SSB web site by MAS right here.