{kind=link}

With regards to financing your training, understanding the variations between backed vs unsubsidized pupil loans is essential. Each forms of loans are a part of the federal pupil mortgage program, designed to assist college students cowl the prices of upper training. Nevertheless, they’ve distinct options that may considerably impression your general monetary burden throughout and after your research.

At Sadek Chapter Regulation Workplaces, we’re devoted to serving to college students in Pennsylvania and New Jersey perceive their mortgage choices and supply them with personalised debt reduction options. You probably have already taken out a backed or unsubsidized mortgage on your training and are overwhelmed by pupil mortgage debt, contact a Philadelphia pupil mortgage debt reduction lawyer at Sadek Regulation right this moment.

Collectively, we may help you discover your choices and discover one of the best path ahead on your academic and monetary future. Name our Pennsylvania quantity at (215) 545-0008 or our New Jersey quantity at (856) 890-9003 to schedule a free session with a member of our workforce concerning your scenario.

What Is the Federal Direct Mortgage Program?

The William D. Ford Federal Direct Mortgage Program (also called the Direct Mortgage Program) is a U.S. authorities initiative that gives low-interest pupil loans to assist cowl the price of greater training. In contrast to non-public loans, these loans are issued immediately by the federal authorities by means of the Division of Schooling, they usually are available varied types, together with Direct Backed Loans and Direct Unsubsidized Loans.

This program affords versatile reimbursement choices and is designed to make school extra accessible to people with a higher monetary want.

What Is FAFSA?

FAFSA, or the Free Utility for Federal Scholar Help, is a web-based kind that college students within the U.S. should fill out to use for monetary assist for school or graduate faculty. It helps decide a pupil’s eligibility for federal grants, loans, and work-study applications, in addition to some state and institutional assist.

When you apply for FAFSA, your faculty’s monetary assist workplace will use the monetary data you’ve supplied to calculate how a lot assist you’re eligible to obtain primarily based in your monetary wants.

Federal Scholar Loans {Qualifications}

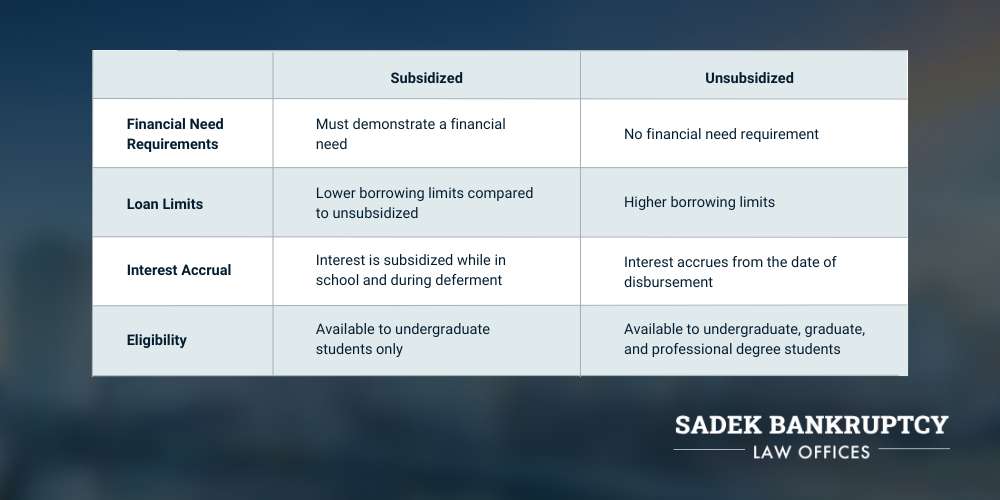

With a purpose to decide which mortgage is best for you, it’s essential to know which mortgage you really qualify for. Beneath are the qualifying standards for backed and unsubsidized loans.

Backed loans require debtors to reveal monetary want, whereas unsubsidized loans do not need a monetary want requirement. Moreover, the federal authorities pays the curiosity on backed loans whereas the borrower is in class or throughout deferment, whereas unsubsidized loans accrue curiosity from the second they’re disbursed.

Direct backed loans typically have decrease borrowing limits in comparison with direct unsubsidized loans, which supply greater most limits. This enables unsubsidized loans to accommodate a broader vary of academic bills. Lastly, backed loans are solely obtainable to undergraduate college students. In distinction, unsubsidized loans can be found to undergraduate college students, graduate college students, {and professional} diploma college students.

What Are the Most Borrowing Limits for the Federal Direct Mortgage Program?

The Direct Mortgage Program units annual and lifelong borrowing limits primarily based on a pupil’s yr in class and their dependency standing. For dependent undergraduate college students, the utmost annual mortgage restrict ranges from $5,500 for first-year college students to $7,500 for third-year college students and past. Unbiased undergraduates can borrow extra, with annual limits starting from $9,500 to $12,500.

Graduate or skilled pupil debtors have a better annual restrict of $20,500 for unsubsidized loans. The overall borrowing restrict for undergraduates is $31,000 for dependents and $57,500 for independents, whereas graduate college students can borrow as much as $138,500. The graduate mixture borrowing restrict additionally contains any loans they acquired throughout their undergraduate profession.

What Is the Distinction Between Backed and Unsubsidized Loans?

With regards to financing training, understanding the distinction between backed vs unsubsidized pupil loans is important for making knowledgeable selections. Each forms of loans are supplied by means of the federal authorities, however they cater to completely different monetary wants and circumstances.

Beneath we’ll discover every mortgage kind in additional element, serving to you identify which choice could also be best for you.

Backed Loans

First, we’re going to speak about backed pupil loans, their qualifying necessities, and their important benefit over unsubsidized pupil loans.

Direct Backed Mortgage

Direct backed loans are a kind of federal pupil mortgage supplied by means of the Direct Mortgage Program. These loans are solely obtainable to undergraduate college students, and with the intention to qualify, it’s essential to reveal a monetary want.

The principle benefit of those loans is that the U.S. Division of Schooling covers the curiosity on the mortgage when you are enrolled in class at the least half-time, throughout the six-month grace interval after leaving faculty, and through your deferment interval. This makes them extra inexpensive than loans the place curiosity accumulates instantly, like direct unsubsidized loans.

Do Backed Loans Have Curiosity?

Sure, backed loans do have curiosity, however the U.S. Division of Schooling covers it whereas the coed is enrolled at the least half-time, throughout the six-month grace interval after leaving faculty, and through deferment durations.

Unsubsidized Loans

Subsequent, we’re going to debate unsubsidized federal pupil loans and the way they examine to backed loans.

Direct Unsubsidized Mortgage

Direct unsubsidized loans are federal loans which can be obtainable to undergraduate, graduate, {and professional} college students. Moreover, they are often granted to college students no matter their monetary want.

In contrast to backed loans, curiosity on unsubsidized loans begins accruing as quickly because the mortgage is disbursed. These loans provide versatile reimbursement choices however include the added value of accumulating curiosity all through the borrowing interval.

Do Unsubsidized Loans Have Curiosity?

Sure, unsubsidized loans have curiosity, and it begins accruing from the second the mortgage is disbursed. In contrast to backed loans, the federal government doesn’t cowl the curiosity at any level.

Whereas college students can defer curiosity funds whereas in class, any unpaid curiosity will capitalize, which means it will get added to the principal steadiness, which will increase the overall quantity that should be repaid over time.

Understanding Compensation of Backed and Unsubsidized Loans

The reimbursement interval for backed and unsubsidized loans usually begins six months after commencement, leaving faculty, or dropping under half-time enrollment, also called the grace interval. For backed loans, the federal government covers the curiosity throughout this grace interval, whereas for unsubsidized loans, curiosity begins accruing instantly, which means debtors could owe extra as soon as reimbursement begins.

Each forms of loans provide a number of reimbursement plans, together with normal, graduated, and income-driven choices, permitting debtors to decide on a plan that most closely fits their monetary scenario. It’s essential for debtors to speak with their mortgage servicer and keep knowledgeable about reimbursement choices to handle their debt successfully and keep away from potential default.

At Sadek Chapter Regulation Workplaces, our skilled chapter legal professionals perceive the challenges that include repaying backed and unsubsidized pupil loans. When you’re struggling to satisfy your mortgage obligations, we will information you thru the choices obtainable to alleviate your monetary burden.

Our workforce will assess your particular person scenario, offering personalised recommendation on whether or not chapter may be a viable answer. Whereas pupil loans are usually not dischargeable in chapter, sure circumstances—resembling proving undue hardship—can result in reduction.

We’ll allow you to discover income-driven reimbursement plans, mortgage consolidation, or deferment choices to handle your funds extra successfully. If chapter is suitable, our attorneys will work diligently to organize and current your case, advocating on your greatest pursuits and aiming for probably the most favorable final result doable.

What Are the Execs and Cons of Backed and Unsubsidized Scholar Loans?

Each backed and unsubsidized loans include their very own set of benefits and drawbacks. When deciding between the 2, it’s essential to weigh these professionals and cons to seek out the mortgage that’s best for you. Beneath are the professionals and cons of backed vs unsubsidized loans.

Execs of Backed and Unsubsidized Loans

Listed here are some key professionals for every kind of mortgage:

Execs of Backed Loans

- No curiosity accrual whereas in class, lowering the general value of the mortgage.

- Decrease rates of interest in comparison with unsubsidized loans.

- Monetary want necessities forestall debtors from taking out federal pupil loans they don’t want.

Execs of Unsubsidized Loans

- No monetary want necessities, which may make them extra accessible to debtors.

- Larger borrowing limits, which may enable college students to borrow extra annually.

- Versatile reimbursement choices to select from, together with choices that may accommodate varied monetary conditions.

Cons of Backed and Unsubsidized Loans

In distinction, listed below are a few of the cons of every kind of mortgage:

Cons of Backed Loans

- Solely undergraduate college students with demonstrated monetary want qualify, which can exclude some debtors.

- Decrease annual and lifelong borrowing limits in comparison with unsubsidized loans, which may doubtlessly require further borrowing.

- Rates of interest can change, impacting the general value if charges enhance throughout the mortgage time period.

Cons of Unsubsidized Loans

- Curiosity begins accumulating instantly, which may result in a bigger complete reimbursement quantity over time.

- Larger rate of interest prices in comparison with backed loans.

- Potential for debt accumulation attributable to ease of entry, leading to greater debt burdens.

In conclusion, understanding the potential upsides and disadvantages of each backed and unsubsidized loans is essential for you as you propose your training financing. Evaluating these professionals and cons may help you make knowledgeable selections about which mortgage sorts greatest align along with your monetary scenario and long-term targets.

Backed and Unsubsidized Mortgage FAQs

Which Mortgage Sort Gives Curiosity Subsidy?

Backed loans offer you an curiosity subsidy. With these loans, the U.S. Division of Schooling pays the curiosity whereas the coed is enrolled at the least half-time, throughout the six-month grace interval after commencement, and during times of deferment.

This function helps cut back the general value of borrowing in comparison with unsubsidized loans, the place curiosity accrues from the time the mortgage is disbursed.

Do You Need to Pay Again Unsubsidized Loans?

Sure, you do should pay again unsubsidized loans. Debtors are answerable for the complete quantity borrowed, plus any curiosity that has accrued from the time the mortgage is disbursed. Whereas college students can select to defer funds whereas in class, any unpaid curiosity will capitalize.

This implies it will get added to the principal steadiness, which may enhance the overall quantity owed over time. It’s essential to know the reimbursement phrases and plan accordingly to handle this debt successfully.

When Do Unsubsidized Loans Accrue Curiosity?

Unsubsidized loans accrue curiosity from the second they’re disbursed. Which means curiosity begins accumulating instantly, no matter whether or not the coed is enrolled in class or in a deferment interval.

In contrast to backed loans, the place the federal government covers curiosity whereas the coed is in class, debtors of unsubsidized loans are answerable for paying the coed mortgage curiosity all through the lifetime of the mortgage, together with during times of enrollment.

Are Backed Loans Curiosity-Free?

No, backed loans aren’t interest-free. The coed should make all remaining curiosity funds on their mortgage after they graduate, drop out, or are in any other case not enrolled in class at the least half-time, after their six-month grace interval after commencement is up, and/or after they’re not in deferment.

Whereas backed loans have decrease prices throughout faculty, they usually provide vital curiosity advantages, they do ultimately incur curiosity as soon as reimbursement begins.

Ought to I Pay Off Backed or Unsubsidized Loans First?

Usually, it’s best to repay unsubsidized loans first. Since unsubsidized loans accrue curiosity from the second they’re disbursed, they will change into dearer over time attributable to accumulating curiosity.

Paying off these loans first may help reduce general curiosity prices. Nevertheless, you probably have a particular monetary scenario, resembling income-driven reimbursement plans or forgiveness choices, take into account these components in your resolution.

In the end, prioritizing loans with the very best rates of interest generally is a sound technique to cut back debt extra successfully. At Sadek Chapter Regulation Workplaces, we will consider your scenario and advise you on one of the best plan of action concerning your federal pupil loans.

Contact a Scholar Mortgage Chapter Legal professional in Pennsylvania and New Jersey at Sadek Regulation

When you’re struggling along with your current federal loans and contemplating your choices for debt reduction, contact the Pennsylvania and New Jersey attorneys at Sadek Chapter Regulation Workplaces right this moment. We perceive that the burden of pupil loans can really feel overwhelming, particularly when you find yourself attempting to construct a steady monetary future.

Our skilled workforce is devoted to serving to our shoppers discover their rights and potential options for managing their pupil mortgage debt. Whether or not you’re coping with federal or non-public pupil loans, we will offer you the authorized choices that you must search reduction from overwhelming debt and creditor harassment.

Scholar mortgage chapter generally is a viable choice for individuals who qualify, however the course of might be difficult with out professional steerage. Our attorneys are well-versed within the nuances of pupil mortgage legal guidelines and may help you assess your scenario to find out one of the best plan of action. You probably have questions on pupil mortgage debt reduction or need to get began with us right this moment, name our legislation agency to schedule a session with us.

Pennsylvania residents can name us at (215) 545-0008, and New Jersey residents can name us at (856) 890-9003. You can even contact us on-line through our web site to schedule your free session with a debt reduction lawyer on our workforce.

{

“@context”: “https://schema.org”,

“@kind”: “FAQPage”,

“mainEntity”: [{

“@type”: “Question”,

“name”: “What Is the Federal Direct Loan Program?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “The William D. Ford Federal Direct Loan Program (also known as the Direct Loan Program) is a U.S. government initiative that provides low-interest student loans to help cover the cost of higher education.”

}

},{

“@type”: “Question”,

“name”: “What Is FAFSA?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “FAFSA, or the Free Application for Federal Student Aid, is an online form that students in the U.S. must fill out to apply for financial aid for college or graduate school. It helps determine a student’s eligibility for federal grants, loans, and work-study programs, as well as some state and institutional aid.”

}

},{

“@type”: “Question”,

“name”: “What Are the Maximum Borrowing Limits for the Federal Direct Loan Program?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “For dependent undergraduate students, the maximum annual loan limit ranges from $5,500 for first-year students to $7,500 for third-year students and beyond. Independent undergraduates can borrow more, with annual limits ranging from $9,500 to $12,500. Graduate or professional student borrowers have a higher annual limit of $20,500 for unsubsidized loans. The total borrowing limit for undergraduates is $31,000 for dependents and $57,500 for independents, while graduate students can borrow up to $138,500.”

}

},{

“@type”: “Question”,

“name”: “What Is the Difference Between Subsidized and Unsubsidized Loans?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “The main difference between subsidized and unsubsidized student loans is that subsidized loans do not accrue interest while the borrower is in school or during deferment periods, whereas unsubsidized loans begin accruing interest as soon as they are disbursed.”

}

},{

“@type”: “Question”,

“name”: “Do Subsidized Loans Have Interest?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “Yes, subsidized loans do have interest, but the U.S. Department of Education covers it while the student is enrolled at least half-time, during the six-month grace period after leaving school, and during deferment periods.”

}

},{

“@type”: “Question”,

“name”: “Do Unsubsidized Loans Have Interest?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “Yes, unsubsidized loans have interest, and it begins accruing from the moment the loan is disbursed. Unlike subsidized loans, the government does not cover the interest at any point.”

}

},{

“@type”: “Question”,

“name”: “Which Loan Type Provides Interest Subsidy?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “Subsidized loans provide you with an interest subsidy. With these loans, the U.S. Department of Education pays the interest while the student is enrolled at least half-time, during the six-month grace period after graduation, and during periods of deferment.”

}

},{

“@type”: “Question”,

“name”: “Do You Have to Pay Back Unsubsidized Loans?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “Yes, you do have to pay back unsubsidized loans. Borrowers are responsible for the entire amount borrowed, plus any interest that has accrued from the time the loan is disbursed. While students can choose to defer payments while in school, any unpaid interest will capitalize.”

}

},{

“@type”: “Question”,

“name”: “When Do Unsubsidized Loans Accrue Interest?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “Unsubsidized loans accrue interest from the moment they are disbursed. This means that interest begins accumulating immediately, regardless of whether the student is enrolled in school or in a deferment period.”

}

},{

“@type”: “Question”,

“name”: “Are Subsidized Loans Interest-Free?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “No, subsidized loans are not interest-free. The student must make all remaining interest payments on their loan after they graduate, drop out, or are otherwise no longer enrolled in school at least half-time, after their six-month grace period after graduation is up, and/or after they are no longer in deferment.”

}

},{

“@type”: “Question”,

“name”: “Should I Pay Off Subsidized or Unsubsidized Loans First?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “Generally, you should pay off unsubsidized loans first. Since unsubsidized loans accrue interest from the moment they are disbursed, they can become more expensive over time due to accumulating interest.”

}

}]

}

The publish Understanding Backed vs Unsubsidized Scholar Loans appeared first on Sadek Chapter Regulation Workplaces.