{kind=link}

On the floor, JAVA and JGRO look promising. Each ETFs carry Morningstar Medalist Scores of “Silver,” a designation awarded to funds that Morningstar analysts have “excessive conviction will outperform the related index, or most friends, over a market cycle on a risk-adjusted foundation.” That’s not a foul endorsement in the event you belief the judgement behind it. (Gold scores are for the highest 15%, the place as silver scores are for the subsequent 35%.)

JPMorgan additionally promotes the relative historic outperformance of each funds. JAVA, as an illustration, highlights its outcomes versus the Morningstar giant worth class common and the Russell 1000 Worth Index. JGRO equally claims outperformance versus its Morningstar peer class common.

U.S. lively ETFs nonetheless battle to outperform index ETFs

Benchmark comparisons might be rigorously chosen. Morningstar analyst scores, whereas useful, are nonetheless topic to authority bias. This implies individuals might place an excessive amount of belief in professional opinions even when these consultants could also be biased or flawed.

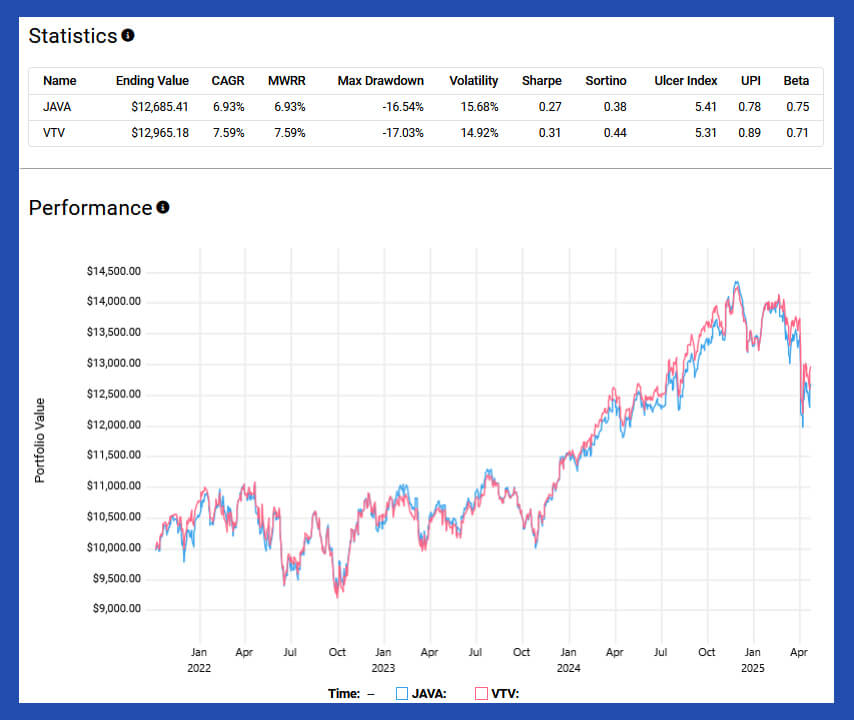

Taking a look at historic returns in contrast on to broadly out there, low-cost U.S. benchmarks paints a extra combined image. From October 5, 2021, via April 23, 2025, JAVA underperformed the favored Vanguard Worth ETF (VTV), returning a 6.93% CAGR in comparison with VTV’s 7.59%.

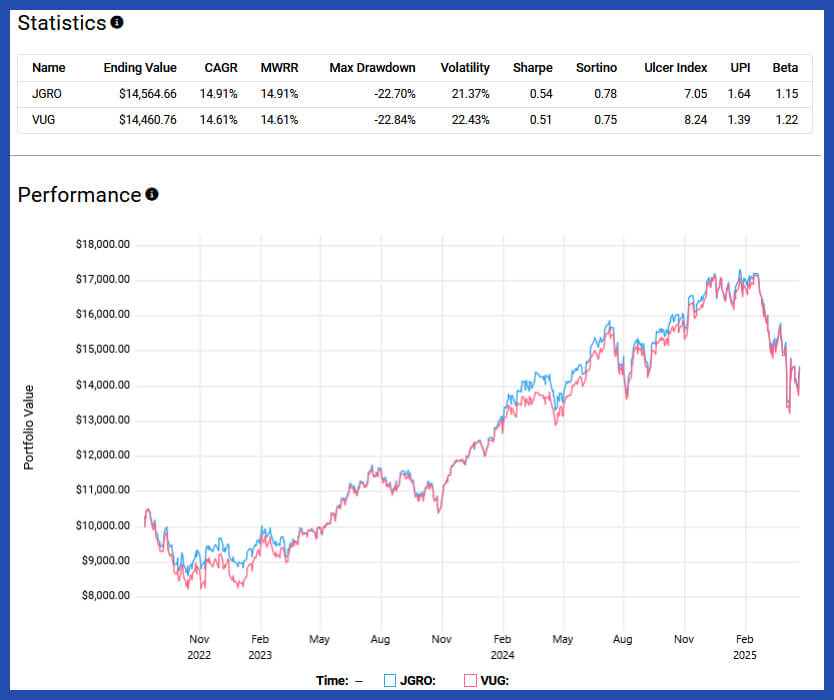

JGRO, however, solely barely outperformed the Vanguard Progress ETF (VUG) over its out there window, returning 14.91% CAGR from August 9, 2022, via April 23, 2025, versus VUG’s 14.61%.

That begs the query: why pay 0.44% for JAVA or JGRO when VTV and VUG supply comparable performing large-cap worth and progress publicity at simply 0.04%? The fee hole is critical, and it turns into even tougher to justify while you study portfolio overlap.

As of April 24, there have been 99 overlapping holdings between JAVA and VTV. That represents 61.5% of JAVA’s 165 holdings, and 30.4% of VTV’s 335 holdings. This degree of overlap suggests a significant diploma of similarity between the 2 portfolios, at the very least when it comes to core holdings.

For JGRO, the overlap is barely decrease however nonetheless notable. It shares 58 holdings with VUG, which quantities to 51.8% of JGRO’s 114 shares and 35.8% of VUG’s 170. Once more, this implies that regardless of the lively mandate, there’s vital frequent floor between JGRO and its index-tracking counterpart.