{kind=link}

Federal pupil loans and personal pupil loans… which is best?

Most colleges, the federal authorities, and even personal lenders advocate taking out federal pupil loans over personal pupil loans.

With federal pupil loans, each pupil will get the identical aggressive price, they arrive with extra versatile compensation plans they usually supply extra choices for deferment, forbearance, and forgiveness.

However there are a couple of instances the place personal pupil loans truly make extra sense. Should you’re unsure which is best for you, take into account these 5 elements.

1. Are you eligible?

Not everybody can qualify for federal pupil loans or personal pupil loans.

To qualify for federal loans, you have to:

- show monetary want for need-based federal pupil help applications;

- be a U.S. citizen or an eligible noncitizen;

- have a sound Social Safety quantity (apart from college students from the Republic of the Marshall Islands, Federated States of Micronesia, or the Republic of Palau);

- be enrolled or accepted for enrollment as a common pupil in an eligible diploma or certificates program;

- be enrolled no less than half-time to be eligible for Direct Mortgage Program funds;

- keep passable tutorial progress in faculty or profession college;

- signal the certification assertion on the Free Utility for Federal Scholar Help (FAFSA) type stating that you just’re not in default on a federal pupil mortgage, you don’t owe cash on a federal pupil grant, and also you’ll solely use federal pupil help for academic functions; and

- present you’re certified to acquire a university or profession college training.

Non-public pupil loans even have necessities that some college students may not be capable to meet and not using a cosigner. Most have minimal revenue and credit score necessities — two issues most undergraduates usually can’t meet on their very own.

Nevertheless it’s doable to discover a lender that’s keen to work with college students who’re beneath 18, attending a faculty that isn’t eligible for federal help, or don’t have the appropriate residency standing to qualify for federal help — so long as you could have a cosigner, that’s. And not using a cosigner, your choices are significantly restricted.

A few of the greatest personal pupil loans are proven within the desk under:

2. Which truly has a greater price?

Federal pupil mortgage charges have been going up over the previous few years.

Based on Federal Scholar Help, the utmost rates of interest are 8.25% for Direct Backed Loans and Direct Unsubsidized Loans made to undergraduate college students, 9.50% for Direct Unsubsidized Loans made to graduate {and professional} college students, and 10.50% for Direct PLUS Loans made to oldsters of dependent undergraduate college students or to graduate or skilled college students.

Should you’re solely eligible for a Graduate or Mum or dad PLUS Mortgage, a personal mortgage may truly value much less. Particularly when you’ve got a cosigner with sturdy private funds — like a credit score rating over 750 and a low debt-to-income ratio.

Nonetheless, PLUS Loans aren’t eligible for as many perks as different forms of federal loans, so that you may not truly be lacking out on a lot by borrowing from a personal lender.

Non-public pupil mortgage charges begin at 3% with no origination charge. Even in case you don’t get the bottom provided price, it might be decrease or near the price of a federal mortgage with a extra aggressive price.

3. How a lot do it is advisable borrow?

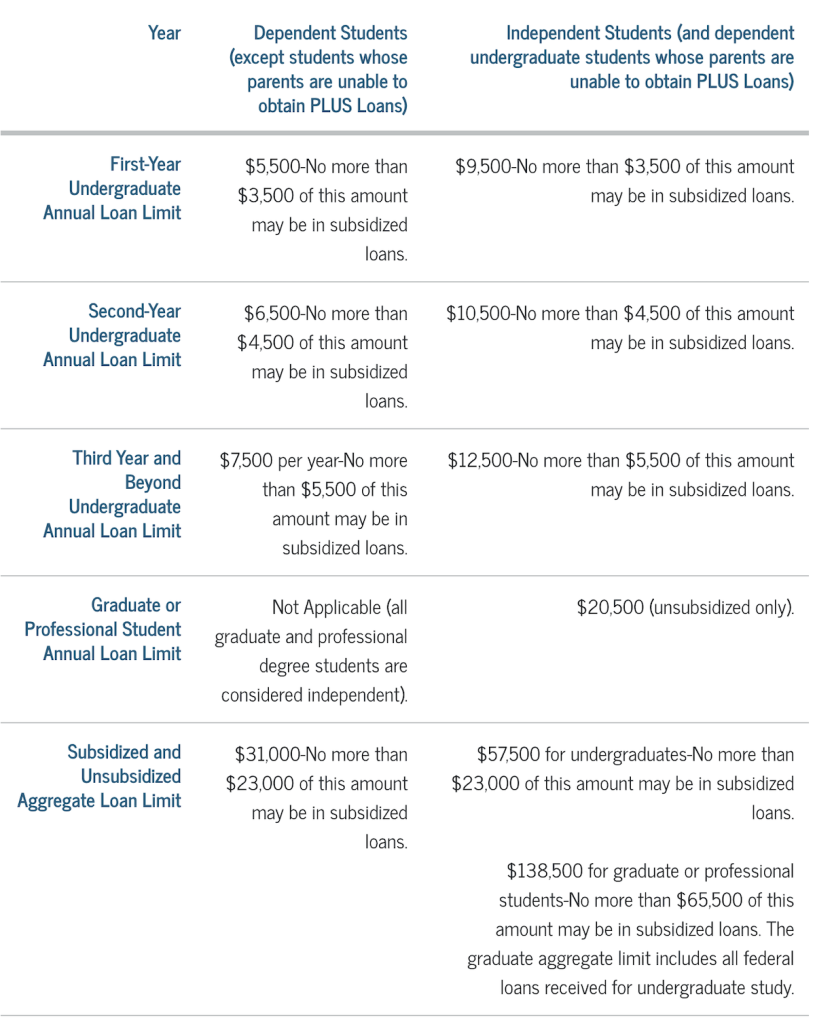

One of many foremost drawbacks to federal pupil loans is that there are limits to how a lot you possibly can borrow for its best applications.

Direct Backed Loans and Direct Unsubsidized Loans are federal pupil loans provided by the U.S. Division of Training (ED) to assist eligible college students cowl the price of greater training at a four-year faculty or college, group faculty, or commerce, profession, or technical college.

These loans is likely to be known as Stafford Loans or Direct Stafford Loans interchangeably, however please notice that these usually are not the official names for these particular loans.

The quantity you possibly can borrow for college is about by your college, and it can’t be greater than what you want financially.

Probably the most you possibly can borrow by the Federal Direct Mortgage Program as a freshman is between $5,500 and $9,500. And also you’re restricted to borrowing $57,500 as an undergraduate and $138,500 as a graduate or skilled pupil.

Whereas $138,500 may sound like so much, it isn’t in case you’re getting a medical diploma or going to regulation college. In these instances, you may not have some other possibility however to borrow from a personal lender — or use a mix of each.

Non-public lenders sometimes have a lot greater limits or assist you to borrow as much as 100% of your school-certified value of attendance.

A notice about the price of attendance

The price of going to varsity doesn’t cease at tuition and costs. Faculties take into account what it calls the price of attendance (COA) when developing along with your monetary help package deal.

Every college has totally different standards for what it considers to be your COA. It often contains housing, meal plans, textbooks and provides, transportation, and different miscellaneous dwelling bills.

Scholar mortgage suppliers are legally not allowed to allow you to borrow greater than your college’s COA. That’s why personal lenders attain out to your college to verify your mortgage quantity if you apply.

4. Are you able to afford to begin paying off your loans whereas in class?

Federal pupil loans usually don’t require you to begin making repayments till six months after you’ve graduated or in any other case dropped under half time — this contains taking a semester off.

Non-public pupil loans don’t all the time supply that luxurious. Or after they do, they provide a number of in-school compensation choices. These typically embrace interest-only repayments, fastened repayments of round $25 or beginning with full repayments immediately.

When you may not be capable to afford full repayments immediately, making small repayments in your mortgage whilst you’re in class might truly enable you save. You are able to do this by getting an internship whereas in faculty or utilizing faculty budgeting apps to save cash every month.

Aside from Federal Direct Backed Loans, curiosity begins including up in your federal loans as quickly as your college receives the funds. Once you lastly begin making repayments, all of that amassed curiosity will get added to your mortgage stability — and also you successfully find yourself paying curiosity on curiosity.

By taking out a personal pupil mortgage and making small repayments early on, you can each save in your whole mortgage value and get out of pupil mortgage debt quicker.

5. What are your plans after commencement?

What you intend on doing after commencement is a particularly essential, albeit unpredictable issue to think about when selecting between federal pupil loans and personal pupil loans.

Undergraduates planning on going to graduate college sooner or later may wish to take into account federal loans, which you’ll defer whilst you’re in class once more. Not all personal lenders enable in-school deferment.

Fascinated by going into public service or working for a nonprofit? You could possibly be eligible for full forgiveness after making 10 years of repayments in your federal loans by the Public Service Mortgage Forgiveness (PSLF) Program.

Actually, anybody contemplating touring round or who thinks they could have a low-income job may wish to select federal loans over personal, since they’re eligible for income-driven repayments. Non-public lenders sometimes solely supply one commonplace compensation plan, and fewer deferment and forbearance choices.

What You Ought to Know About Federal and Non-public Scholar Loans

Touchdown that faculty acceptance letter is barely half the battle in terms of attending greater training — you continue to have to discover a technique to pay for it.

“Larger training has so many challenges, and personal greater training has a particular problem of ever-rising tuition prices”

Ken Starr

It’s true that pupil loans to gasoline your dream of stepping into that Ivy League faculty will certainly assist any pupil kick begin his profession.

Nonetheless, there is no such thing as a denying that the price of greater training has gone from excessive to the best inside a short while span. In some instances, mother and father begin saving each penny simply in order that they will present the essential necessity to their baby which is that of a great faculty training.

There are some who’re in a position to obtain this feat and for individuals who are unable to, there may be the choice of making use of for a federal or personal pupil mortgage.

With one thing like 40 million People juggling pupil mortgage debt, it’s no shock that paying for college with a federal or personal pupil mortgage are widespread methods to deal with these prices.

Earlier than getting too far down the rabbit gap, listed here are six issues to remember:

1. Are pupil loans the one method?

Earlier than a mother or father or a pupil indicators under that dotted line on the phrases and situations of a mortgage software, first, ask your self whether or not making use of for a pupil mortgage is the one method. Individuals assume that the one method by which any pupil will be put by formal highschool training is by taking the extreme burden of a pupil mortgage.

However, in case you look higher and analyze your choices, there are various different alternate options. If a pupil is sharp and has carried out nicely you possibly can apply for a scholarship or some type of grant. Nowadays plenty of universities give you grants and scholarships to draw extra eligible college students to them. All it is advisable do is search extensively and maintain your eyes and ears open for the proper alternative.

2. Will you be capable to pay the scholar mortgage debt again?

In case you are a pupil of 18 years and above and you intend to take a pupil mortgage in your title, you may be the signee and the quantity that should be paid again can even be your duty.

There’s a lot at stake right here and paying again an enormous quantity isn’t so simple as signing that pupil mortgage settlement. So, be very cautious and see in case your funds assist you to pay the financial institution again.

3. Is taking out a pupil mortgage even price it?

Some might ask why that is essential whereas taking a pupil mortgage whether or not or not it’s a federal or personal pupil mortgage. As mentioned within the level above in case you as a pupil are taking a mortgage in your title you’re the one who’s liable to pay it.

If a part of your compensation plan contains your prediction of getting a job after which paying again the quantity, then you definately very nicely be ready and looking out for it. The higher the job you get, the higher will likely be your package deal and it will imply a greater capacity of you to pay again the quantity loaned to you.

4. Are you certain you perceive the scholar mortgage compensation phrases?

Should you see any banking doc on the time of taking a mortgage proper on the backside many issues are written in reasonably smaller texts. Such small texts that they typically go unnoticed. These small texted sentences are literally an important as a result of they cite all of the situations utilized and levied on you.

Earlier than you’re taking any type of pupil mortgage — ensure you perceive all the professionals and cons and in addition perceive what the penalty fees will on account of non-payment. It’s your proper to search out out the speed of curiosity and the compensation schedule so that you just don’t encounter any surprises later. Be cautious reasonably than be sorry.

5. Do you could have some other debt?

Should you or anybody in your loved ones already has one other mortgage taken, then you definately may wish to rethink the choice of taking yet one more mortgage and an added monetary burden. Contemplating if the mortgage quantity is small then most likely there is no such thing as a want to fret, nonetheless, if the quantity is noticeably massive, then the recommendation could be to consider different choices however steer clear of one other pupil mortgage. Individuals typically don’t understand that within the occasion of non-payment their credit score rating will get ruined and it will have an effect on their future mortgage points.

6. Will you retain tabs on the compensation phrases?

Even as soon as you’re taking a pupil mortgage it is vitally essential to maintain a tab on the compensation cycle and maintain an everyday examine on how a lot you could have already paid, and the way a lot of the quantity continues to be left. Should you plan issues proper from day one there will likely be no explanation why it’s possible you’ll encounter an issue like non – fee.

It’s comprehensible that so as to attain your goals folks typically search assist. And, as a pupil, if it’s important to accept making use of for a pupil’s mortgage, take all the required precautions and play it secure. Converse to some advisors (might be your mother and father or somebody identified from the banking sector) and solely then go forward when you discovered what to learn about pupil loans in full.

Federal vs Non-public Scholar Loans Abstract

Ultimately, federal pupil loans are often a extra favorable selection. Non-public pupil mortgage suppliers even are inclined to advocate that you just apply for federal help first earlier than you apply for his or her merchandise.

However in case you can’t qualify for federal help, can get a greater cope with a personal lender or wish to get out of debt as quickly as doable, personal loans might be the way in which to go.

Ascent’s undergraduate and graduate pupil loans are funded by Financial institution of Lake Mills or DR Financial institution, every Member FDIC. Mortgage merchandise might not be out there in sure jurisdictions. Sure restrictions, limitations; and phrases and situations might apply. For Ascent Phrases and Circumstances please go to: www.AscentFunding.com/Ts&Cs. Charges are efficient as of seven/1/2024 and mirror an computerized fee low cost of both 0.25% (for credit-based loans) OR 1.00% (for undergraduate outcomes-based loans). Computerized Fee Low cost is obtainable if the borrower is enrolled in computerized funds from their private checking account and the quantity is efficiently withdrawn from the licensed checking account every month. For Ascent charges and compensation examples please go to: AscentFunding.com/Charges. 1% Money Again Commencement Reward topic to phrases and situations. Cosigned Credit score-Primarily based Mortgage pupil should meet sure minimal credit score standards. The minimal rating required is topic to alter and will rely upon the credit score rating of your cosigner. Lowest APRs require interest-only funds, the shortest mortgage time period, and a cosigner, and are solely out there to our most creditworthy candidates and cosigners with the best common credit score scores.

Faculty Ave Scholar Loans merchandise are made out there by Firstrust Financial institution, member FDIC, First Residents Group Financial institution, member FDIC, or M.Y. Safra Financial institution, FSB, member FDIC. All loans are topic to particular person approval and adherence to underwriting pointers. Program restrictions, different phrases, and situations apply.

(1) Charges proven embrace auto-pay low cost. The 0.25% auto-pay rate of interest discount applies so long as a sound checking account is designated for required month-to-month funds. If a fee is returned, you’ll lose this profit. Variable charges might enhance after consummation. Data marketed legitimate as of 08/01/2023. Variable rates of interest might enhance after consummation. Accepted rate of interest will rely upon creditworthiness of the applicant(s), lowest marketed charges solely out there to probably the most creditworthy candidates and require number of full principal and curiosity funds with the shortest out there mortgage time period.