{kind=link}

The FIRE motion made the rounds in nationwide information for just a few years and nonetheless will get a head nod right here and there.

The FIRE motion made the rounds in nationwide information for just a few years and nonetheless will get a head nod right here and there.

The early retirement (RE) a part of FIRE at all times acquired extra criticism as a result of it’s the aim when somebody doesn’t like their profession selection and desires to flee.

In hindsight, this was me.

Each financially and when it comes to skilled success, you’re higher off discovering a profession from which you don’t wish to retire.

Monetary independence (FI) is tougher to argue in opposition to. Constructing sufficient wealth to allow daring life decisions and monetary freedom is a wholesome aim.

Get there by incomes extra, spending much less, and investing the excess.

The primary criticisms of economic independence are its accessibility and the way lengthy it takes to attain it.

Ranging from zero, it takes not less than a decade to achieve a minimal stage of FI, and realistically longer — particularly lower-wage earners, who might by no means obtain it.

However there’s one other means to take a look at wealth and cash. One which’s accessible to everybody, doesn’t take as lengthy, and nonetheless adheres to the foundational ideas of FIRE.

As an alternative of specializing in monetary independence, try first to strengthen your monetary confidence.

What’s Monetary Confidence?

Monetary confidence is readability in managing your funds and making knowledgeable selections on the trail to attaining long-term monetary targets.

It’s a mix of data, emotional resilience, and planning. It empowers folks to navigate monetary challenges and seize alternatives with out stress or hesitation.

Moreover, it’s the idea in your potential to handle, save, and make investments your cash with out concern or uncertainty, utilizing out there instruments to assist monitor funds and inform selections right now and all through our lifetimes.

There are a number of advantages to constructing monetary confidence:

- Obtain it extra quickly than monetary independence.

- Extra confidence reduces monetary stress and nervousness.

- Higher monetary footing improves relationships.

- Strengthens capabilities to deal with uncertainty.

- Encourages steady studying.

- Results in monetary independence and wealth.

Probably the most vital benefit of economic confidence over monetary independence is its out there to everybody who’s prepared to be taught and inject monetary self-discipline into their lives.

We are able to pursue higher-level long-term targets and significant wealth with confidence as a basis. Monetary confidence is step one towards monetary independence.

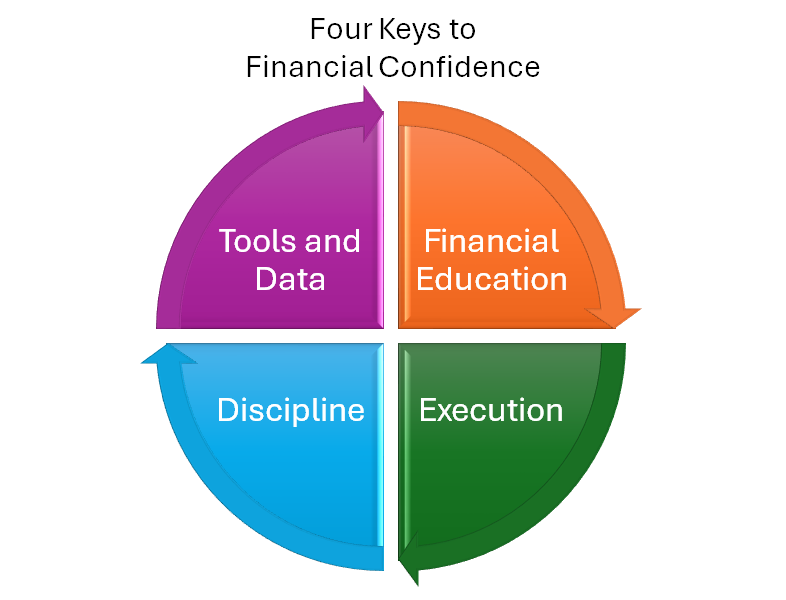

4 Keys to Monetary Confidence

Monetary confidence is tougher to outline than monetary independence.

Monetary confidence is tougher to outline than monetary independence.

Confidence shouldn’t be confused with vanity. Excessive-income earners or belief fund beneficiaries could also be assured as a result of they’re or really feel rich. That’s not what I’m speaking about on this article.

Monetary confidence is for everybody. It’s about sustaining management over your funds and feelings and eliminating concern and trepidation with information.

Those that have it keep disciplined and use knowledge for decision-making to allow them to develop wealth and deal with adversity or uncertainty when it inevitably arrives.

Listed below are 4 keys to unlock monetary confidence.

Monetary Training

The extra you be taught and research about cash, the extra confidently you possibly can handle it. I take this as a right as a result of I used to be a scholar of finance from an early age, earned a Finance diploma, and proceed to be taught and train it right now.

The extra you be taught and research about cash, the extra confidently you possibly can handle it. I take this as a right as a result of I used to be a scholar of finance from an early age, earned a Finance diploma, and proceed to be taught and train it right now.

Dad and mom who train children about cash elevate extra accountable adults. However not everybody has the posh of financially savvy mother and father.

Monetary training in our faculties has improved over the previous twenty years, however it’s inadequate.

Exterior teams like Junior Achievement and Scouting organizations complement the training system with real-life abilities that aren’t prioritized in public center and excessive faculties.

However into maturity, monetary training rests solely on the person.

Monetary educators share their information in books, blogs, enterprise information, neighborhood faculty programs, on-line programs, or wherever folks devour data. Training sources are considerable if we are able to focus amid life’s infiltrating distractions.

Monetary training is the muse of economic confidence, empowering us to execute vital selections about our wealth.

Execution

Cash-smart folks generally know what they’re purported to do however hesitate to behave on what they’ve realized.

Cash-smart folks generally know what they’re purported to do however hesitate to behave on what they’ve realized.

For instance, a financially savvy individual might know they need to be investing extra within the inventory market however don’t improve their employer contributions for concern of a market crash.

Or they know they need to full an property plan however aren’t positive the place to start out, so it stays a perpetual to-do listing merchandise.

They know {that a} lump sum of money in a low-yield checking account could be higher invested elsewhere, however deciding on the correct brokerage, ETF, or high-yield financial savings account is an awesome roadblock.

Retirees acknowledge they will afford to spend extra freely in retirement however can’t let go of their frugal methods.

Monetary information is simply helpful should you execute what you’ve realized. Contribute extra, end the property plan, purchase the ETF, and revel in what you’ve earned. However keep away from the conduct pitfalls that may derail your earlier good cash strikes.

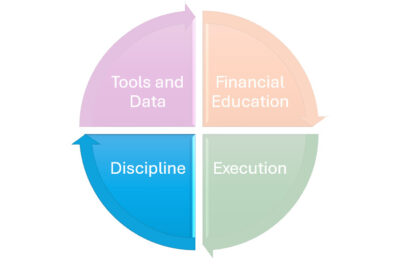

Self-discipline

All of the information on the web can’t overcome the shortage of economic self-discipline.

All of the information on the web can’t overcome the shortage of economic self-discipline.

I lately communicated with a brand new reader who mentioned he was “good at math however traditionally dumb with cash”.

His “dumb with cash” downside led to bank card debt and excessive curiosity funds, despite the fact that he understands the putrid penalties behind paying 29% on an impulse buy.

Excessive revenue doesn’t assure wealth, simply as low revenue isn’t a life sentence for poverty.

Even the ultra-wealthy go bankrupt due to boastful spending or unthoughtful borrowing. Who can resist the temptation of a non-public yacht when you’ve lastly made it?

Retaining what you earn and rising and preserving property builds long-term monetary stability and wealth.

Behavioral reactions to market fluctuations, poor spending habits, or boneheaded purchases can unravel years of excellent selections or the benefits of a excessive revenue.

Monetary instruments and knowledge can assist us keep self-discipline as we navigate financial adjustments and market volatility.

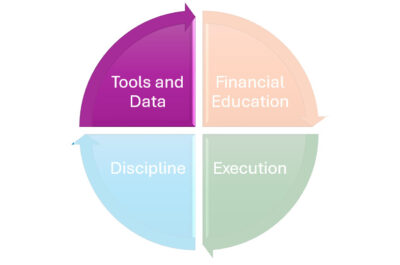

Instruments and Information

We should always all try to run our family financials like a enterprise, constructing a robust stability sheet, diversifying revenue sources, and sustaining wholesome money flows.

We should always all try to run our family financials like a enterprise, constructing a robust stability sheet, diversifying revenue sources, and sustaining wholesome money flows.

Since knowledge informs selections in enterprise, we also needs to use it to make every day selections about our household funds.

Monetary knowledge is available in many kinds, like financial institution and bank card statements and on-line entry to brokerage accounts.

Spreadsheets are the rawest and most customizable instruments.

However too usually, Frankenstein spreadsheets change into a time suck once we might be utilizing our efforts to extract precious insights from higher, current instruments.

I nonetheless use spreadsheets, however I’m gravitating towards solely utilizing software program instruments to make data-driven selections. These present structured enter and output codecs related to everybody’s wants and aligned with tax legal guidelines and monetary planning requirements.

Listed below are the instruments I’m utilizing and recommending now:

- Boldin (overview) — Boldin calls itself the “monetary confidence platform” and was the inspiration for the title of this weblog put up. It’s highly effective DIY monetary planning software program to get good about your cash right now and into the longer term. It lately rebranded from NewRetirement. Attempt it free for 14 days.

- ProjectionLab (overview) — A DIY monetary planning platform that takes inputs and tasks forward-looking visualizations to assist us plan and determine.

- Lunch Cash — A easy desktop budgeting app that’s higher than Mint ever was, with out all of the advertisements. The primary month is free.

- Empower — Free web price calculator and portfolio monitoring account aggregator. Nonetheless beneficial, however previous its glory days.

The primary three on this listing are paid merchandise providing full-functioning free trials of various lengths.

Boldin and ProjectionLab are comparable instruments with acquainted visualizations. Boldin is a extra linear expertise, whereas ProjectionLab has a extra trendy look and freestyle strategy. Boldin helps you to hook up with exterior accounts, whereas ProjectionLab depends on guide inputs (which some might favor).

Sadly, the “freemium” fashions deployed by the now-defunct Mint.com and nonetheless utilized by Empower are masked as lead mills. Mint went below, and Empower has change into irritating to make use of, proving that free will not be at all times a sustainable mannequin.

Most customers are accustomed to paying for companies like newspaper subscriptions to get a cleaner expertise with out turning into the product themselves.

Monetary instruments have gone in that path, too. I favor to pay a small quantity per 12 months to get extraordinary worth out of economic instruments.

The merchandise above value $9-$12 per 30 days, which is about the price of a elaborate dinner with a partner or pal. However these present great suggestions and knowledge to assist drive monetary selections about spending, investing, and drawing down retirement property.

Use monetary instruments and knowledge to information you and deepen your monetary know-how.

Conclusion

Monetary confidence is the brand new monetary independence.

Whereas monetary independence stays a fascinating aim, it could possibly appear distant or unattainable for a lot of. It can be elusive and are available and go because the market fluctuates.

Then again, monetary confidence is an achievable mind-set for anybody prepared to be taught, implement finest practices, and constantly refine their information. Although private finance will be humbling, instruments can assist you keep sane and balanced alongside the way in which at a fraction of the price of skilled recommendation.

It empowers people to make knowledgeable selections, deal with monetary challenges with readability, and finally construct a path towards monetary independence and sustainable wealth.

Featured photograph through DepositPhotos used below license.

Craig Stephens

Craig is a former IT skilled who left his 19-year profession to be a full-time finance author. A DIY investor since 1995, he began Retire Earlier than Dad in 2013 as a artistic outlet to share his funding portfolios. Craig studied Finance at Michigan State College and lives in Northern Virginia along with his spouse and three youngsters. Learn extra.

Favourite instruments and funding companies proper now:

Boldin — Spreadsheets are inadequate. Construct monetary confidence. (overview)

Certain Dividend — Analysis dividend shares with free downloads (overview):

Fundrise — Easy actual property and enterprise capital investing for as little as $10. (overview)

M1 Finance — A high on-line dealer for long-term buyers and dividend reinvestment. (overview)